PLEASE CLICK HERE TO SUBSCRIBE TO MY YOUTUBE CHANNEL @MoneyWithJames

#Money #Education #StockMarket #RealEstate #Learning #Finance #Investing #Learn #Wealth

What is the most important concept to understand in money and wealth creation…?

You could argue there are many important concepts but most people, including me, would say understanding and utilising compounding is that key concept. So what is compounding? Why is it so important? And how can YOU take advantage of it? These are some of the questions I will discuss today. And stick around to the end, as I identify some truly fascinating numbers for you to remember to help build financial security for you or your children.

Remember when you were in school, perhaps some of you watching this still are, and your math teacher tried to teach you about something called EXPONENTIAL GROWTH or an exponential curve? So while I think schooling, sadly, is massively neglecting financial education for most of us around the world, understanding exponential growth might be the most important concept to understand, in money and wealth creation, that we are actually taught about in schools. So for those currently scratching their heads what is exponential growth?It is the magical growth which affects both the natural world in things like the spread of a virus (remember the rapid spread of COVID!) or population growth, but most importantly for this channel, is its magical power for investment returns. Said another way, it is… growth on growth… which means the rate of change becomes more and more dramatic over time creating a J-shaped curve.

Why is exponential growth so relevant for investment returns? It is because the concept of this post/video, compounding, is an exponential concept. That is, when your little money soldiers go out working for you and bring back more money soldiers and then they go out and bring back more money soldiers and more and more and more.

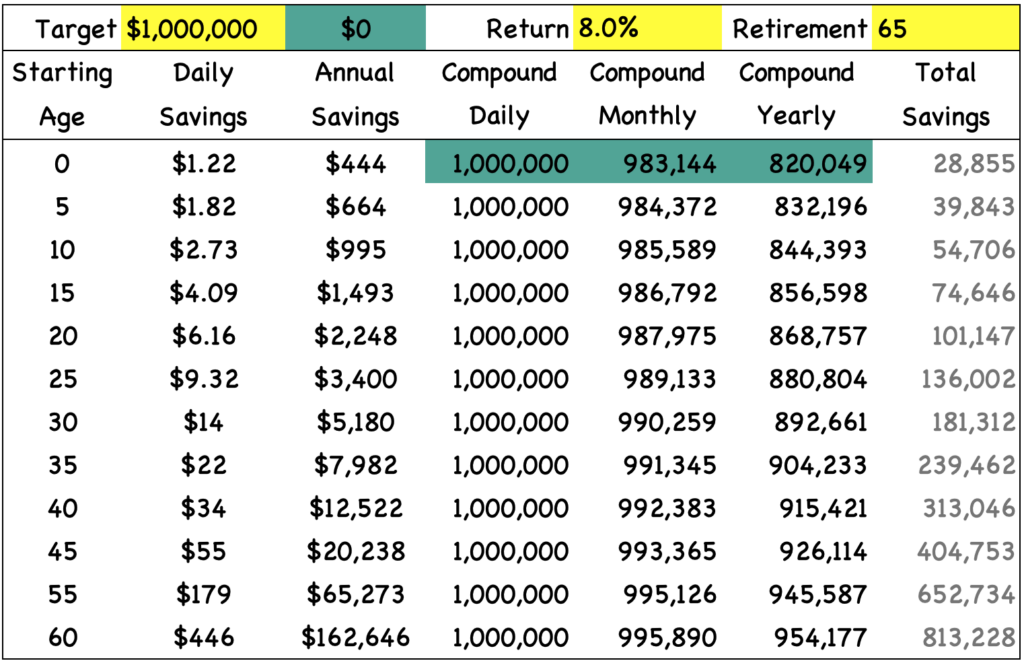

I will explain this another way, imagine you wanted one million dollars by the time you get to 65 (typical retirement age).

If you start to save when you turn 20 years old you will need to save just over $6 every day (and how much would you have actually contributed over those 45 years, from 20 to 65? Due to the magic of compounding, your personal contributions are just $100,000 over those 45 years, you would therefore make $900,000 for free (in growth and most importantly growth on growth on growth). That is why compounding is magic!

And for all parents, or future parents watching, how much would you need to contribute at the birth of each child to give them $1M at retirement age? Just over $1 a day, so you could in theory start them off contributing $1 a day and when they get to 25 they can simply continue at $1 a day until their retirement. And if you can contribute $6 a day from birth then your baby will have $5M at retirement.

Now all of these examples are assuming 8% annual return compounded daily, which is a great interest-bearing return but somewhat conservative in a growth asset like the S&P500, which has returned around 12% annually (when reinvesting dividends) over the past 50 years, although if you adjust for inflation, then 8% compounded is a better reference return for purchasing power. That said, if we therefore assume a 12% return the daily contribution drops to under $0.15 for $1M and at just $1 saved per day from birth, you would have $7.5M at retirement. Contributing just $24,000 over 65 years and due to the magic of compounding make over $7.475M for free!

So what is the missing piece of this puzzle that I have not clearly highlighted yet…?

Well hopefully many of you have guessed already, it is TIME! Compounding’s magic is truly highlighted by time, but it is also built on rate of return and compounding frequency.

So allow me to explain these concepts further.

Going back to our earlier examples, if you start saving for your $1M of retirement money when get to 40 years old, instead of when you were born or at age 20 as I highlighted already, you will need to save almost $35 a day and contribute over $300,000 in total contributions over the following 25 years – so three times as much from your pocket compared to starting at age 20!

Then compounding frequency, if interest is only paid monthly or worst only paid yearly, then your returns can be significantly affected. I will put up a table and you can see back to our $1M example. Starting when you/your baby is born showing compounding monthly vs daily nets around $17,000 less and yearly vs daily yields around $180k less, as highlighted in green. So be sure to ensure your returns are compounded as frequently as possible. Just like they are in something like the S&P500 (ETF tickers, SPY, VOO, etc.).

Now I hope this makes sense for everyone, comment below if you would like me to explain anything, but as you can see just over $1 a day from birth requires a total savings contribution of under $30k over 65 years. Compared to starting at 40 years of age you need to contribute $35 a day and a total savings contribution of over $300k so 10 times as much, which is quite a big difference just by starting earlier and using the magic of compounding! What this table also shows you is the daily amount you would need to save from whatever age you currently are to get to retirement with $1M.

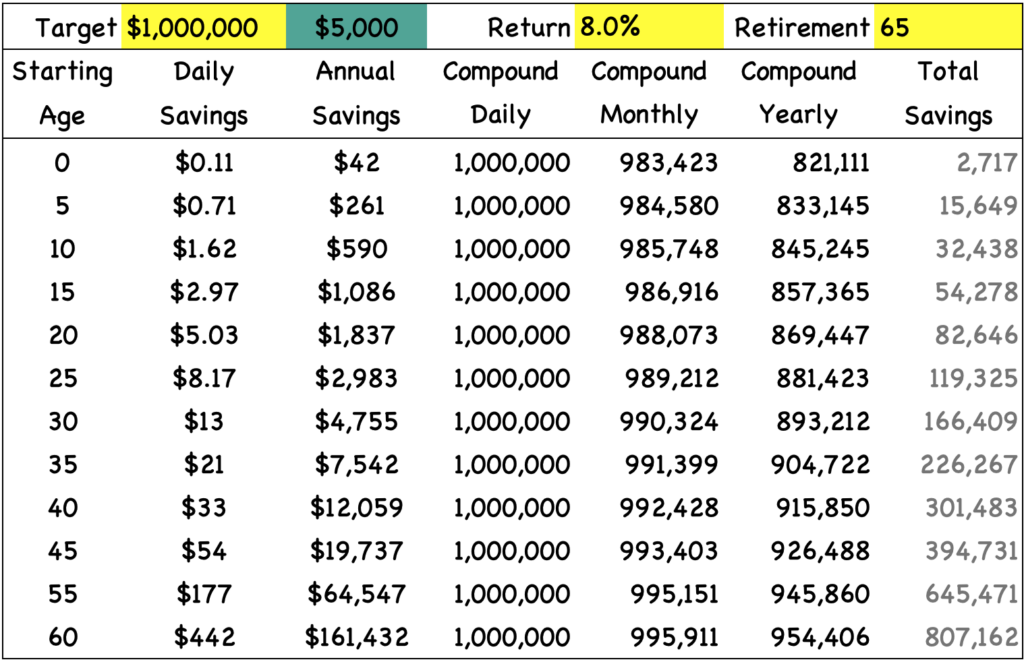

Here’s another table, comparing the $1M retirement target to if you started with $5,000 invested at the beginning. You basically do not need to contribute anything, which may make you ask how much do you need to start with to get to $1M after 65 years without any more contributions…? Can you guess…?

That number is $5,520 at 8%.

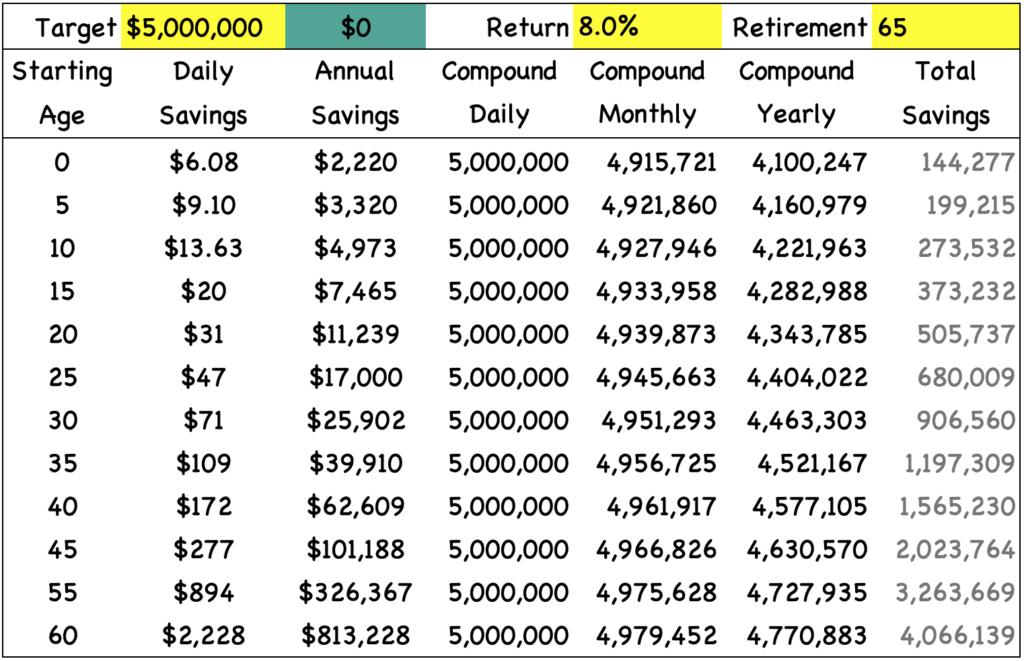

Here’s another table, aiming for a $5M retirement target…

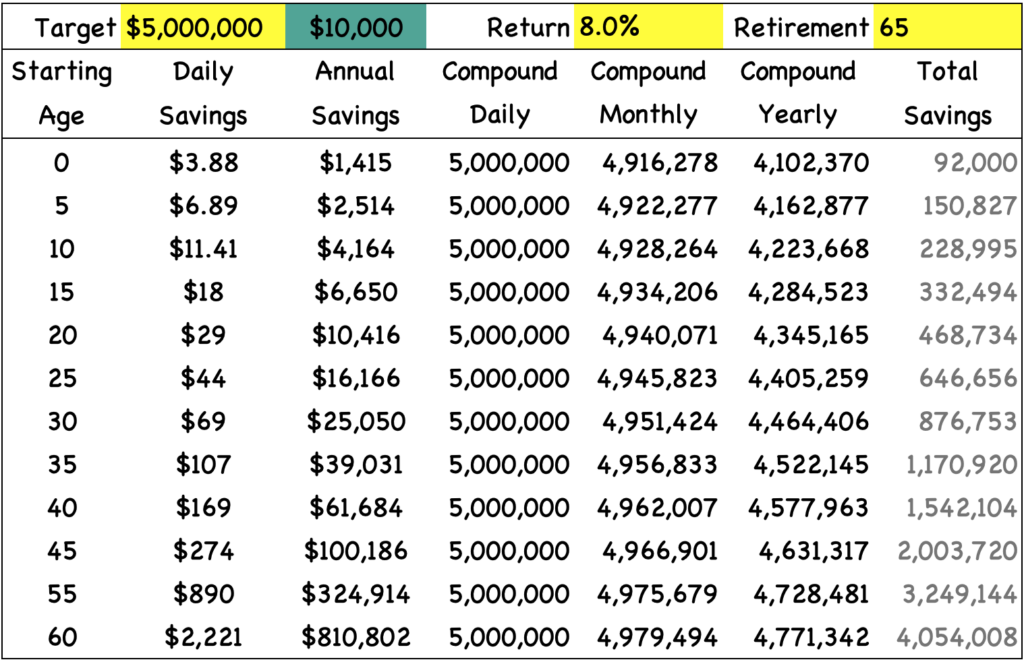

and this time comparing it to starting with $10,000 invested at the beginning. You can see the huge impact.

And now I bet some of you are asking what that magical upfront amount would be if you were earning the average 12% S&P500 return? Meaning if you invest just this amount at the birth of each of your children into the S&P500 and the S&P500 continues to return 12% per year by the time they reach 65 they will have $1M dollars. How much do you think that amount would be…?

Please guess, it is under $500 upfront. It is worth saying that with inflation, sadly $1M by then is unlikely worth much in real terms, so how about $5M? Before I say it, please do guess, as I am confident you will be amazed. How much will you need to invest at the birth of each of your children for them to each have $5M at age 65 for retirement…?

It is just over $2,000, yep! $2,050 to be more precise. I know that may be lot for many but it is far lower than I assume most of you guessed. It is basically the price of a new iPhone or laptop. So consider that.

And just in case you think $5M is not enough, how about we do the same guess for $10M, please do guess, as it helps with your learning and highlighting this really is magic…

Just over $4,000. $4,102 to be precise. So if you can find a few thousand dollars at the birth of your children and invest it in a low cost S&P500 index tracker, reinvesting all dividends, then by the time they come to retirement age they will have millions to rely on. This really is the magic of compounding your returns combined with time.

And if you simply wish to get your children off to a good start for college or to buy a car or a deposit for a house, that same $4,102 invested at birth would have grown to around $35k by the time they are 18 years old, which is nothing like the $10M by age 65, but this is the magic of compounding, with more time the returns grow exponentially. So if you wanted to give your children say $200k by the time they are 18, to have a great start on paying for college, or a house deposit and a car, you would need to invest $25k at birth in a low cost S&P500 index tracker, then let the magic of compounding work. Or if $25k upfront is too much, with regular contributions, you can start with $10k at birth and add $40 a week until they are 18, which is just $2,080 per year – so about the price of two iPhones (which would be a total of $37.5k contributions including the initial $10k). This is the power of compounding by using growth assets and starting early!

Finally, showing it graphically, as you can see from the following chart, back to the $1M example, the red line shows your total savings contributions (just $30k over 65 years), the blue line shows your annual return earned each year if you were to withdraw that return (dividend, interest, etc.) instead of reinvesting it. What is the beautiful green line showing us? The magical exponential J-curve is just so beautiful right? The green line shows the total value if you reinvested the interest and earned interest on your interest or dividends on dividends or growth on growth. Meaning, your newly earned money soldiers (your interest) go back to work for you and earn more money soldiers.

So the overwhelming key is to start as early as possible with as much as possible upfront, then compound your returns, in other words, keep your returns (dividends, interest, etc.) reinvesting and happily ride the beautiful exponential return curve!

So that’s the key concept for today’s post/video. Perhaps basic for some but then it’s just a great reminder of one of the fundamentals and for others this is one of the most foundational concepts to embrace in all of investing.

Leave a Reply